Deposit Protection Scheme

What is a deposit protection scheme (DPS)?

A deposit protection scheme protects depositors by paying compensation to them in the event of a bank failure. In Hong Kong, the DPS is established under the Deposit Protection Scheme Ordinance (DPS Ordinance). In case a member bank of DPS (Scheme member) fails, the DPS will pay compensation up to a maximum of HK$800,000 to each depositor of the failed Scheme member.

When did the DPS in Hong Kong commence operation?

The DPS in Hong Kong commenced operation on 25 September 2006.

Who operates the DPS?

The DPS is operated by the Hong Kong Deposit Protection Board (the Board). The Board is an independent statutory body established under the DPS Ordinance.

Do I need to pay for the protection under the DPS?

No, you do not need to pay for the protection under the DPS. The DPS is funded by contributions paid by Scheme members to the Board.

Do I need to apply for protection under the DPS?

No. You do not need to make any application for protection under the DPS.

Is the DPS subsidised by the Government? Does the Government provide any subsidy to the DPS?

No. The DPS is funded by contributions paid by Scheme members.

What is the size of the DPS Fund? Is it sufficient for paying compensation to depositors when a bank failure occurs?

The target size of the DPS Fund is 0.25% of the aggregate amount of protected deposits in the banking sector. The Board has secured a credit facility from the Exchange Fund which is sufficiently large for the purpose of paying compensation to depositors in the event of a bank failure.

How is the DPS Fund managed?

The DPS Ordinance has set out clear guidance on how the DPS Fund should be managed. The Fund can only be invested in deposits with the Exchange Fund, Exchange Fund Bills, US Treasury Bills, and other investments approved by the Financial Secretary.

How frequent does the Board collect contributions from Scheme members?

The Board collects contributions from Scheme members on an annual basis.

Hong Kong Deposit Protection Board

Does the Board regulate banks in Hong Kong? What are the functions of the Board?

No. The Board does not regulate banks in Hong Kong. Its main responsibilities are to collect contributions from Scheme members, invest the funds collected from Scheme members, make compensation to depositors when a Scheme member fails and recover compensation paid to depositors from the liquidator of the failed Scheme member.

Who are members of the Board? Who appoint them?

The Board currently has nine members (with seven non-official members and two ex-officio members). The non-official members are appointed by the Financial Secretary under the delegated authority of the Chief Executive. Please refer to the Composition of the Board for details.

Do members of the Board receive any remuneration?

No.

Who is responsible for monitoring the operation of the Board? To which authority is the Board accountable?

The Board is an independent statutory body established under the DPS Ordinance. The Board is required under the DPS Ordinance to submit its budget to the Financial Secretary for approval every year. Its annual report and financial statements must be audited and laid before the Legislative Council for public scrutiny.

How does the Board perform its functions? How many staff members does the Board have?

The Board is required under the DPS Ordinance to perform functions through the HKMA, unless it is otherwise directed by the Financial Secretary. The Board has around 20 staff members. Most of them are HKMA staff seconded to assist the Board to perform its functions.

Scheme members

Who are members of the DPS?

What institutions are covered by the DPS? How can I distinguish between members and non-members of the DPS?

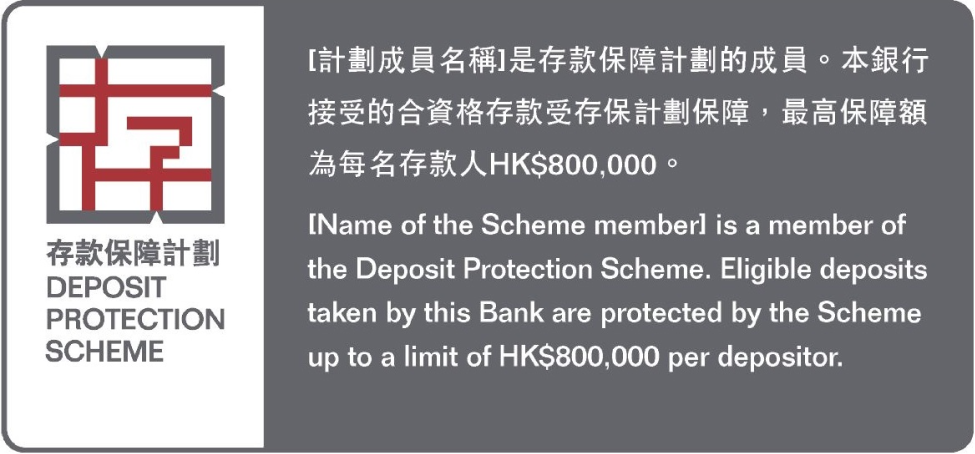

All licensed banks, unless exempted by the Board, are covered by the DPS. A Scheme member is required to display a DPS membership sign prominently at its places of business (for example, bank branches) and the simplified membership sign on its electronic banking platforms.

Which banks are exempted by the Board?

Are restricted licence banks and deposit-taking companies covered by the DPS?

No. Only licensed banks are covered by the DPS.

Are other financial institutions such as securities companies and insurance companies covered by the DPS?

No. Only licensed banks are covered by the DPS.

Level of protection

What is the level of protection available under the DPS?

The maximum level of protection under the DPS is HK$800,000 per depositor per Scheme member.

Why is the protection limit set at HK$800,000? How is it compared to other major economies?

Under the protection limit of HK$800,000, more than 92% of depositors have their deposits fully covered. This level of coverage is in line with international standards. Moreover, the current level of protection limit in Hong Kong is higher than the prevailing levels in many other Asian economies, while comparable to those in the European economies.

If a bank fails, what would happen to that part of my deposit in excess of HK$800,000? Will I be compensated in any way for the excess portion?

A depositor is entitled to make a claim for the remaining balance of his/her deposit in the liquidation of the failed Scheme member.

Will I have more protection if I divide my deposit and maintain it with different banks?

Yes. You will have more protection under the DPS.

If I have a personal account and a limited company account, will both accounts be protected up to a maximum of HK$800,000?

Yes. Each separate legal entity will be protected up to a maximum of HK$800,000.

Depositors protected

Are companies protected by the DPS?

Yes. Both personal and corporate depositors are protected by the DPS.

If I have a joint account with my spouse, are both of us protected?

Holders of a joint account are normally deemed to have an equal share in the deposit. Each of them is entitled to compensation up to a maximum of HK$800,000.

Are deposits held by a sole proprietorship protected by the DPS?

Yes. Deposits held by a sole proprietorship are protected by the DPS. Since a sole proprietorship and the sole proprietor are regarded as a single person under the law, the sole proprietorship and the sole proprietor together are entitled to compensation up to a maximum of HK$800,000.

Are deposits held by a partnership protected by the DPS?

Yes. Deposits held by a partnership are protected by the DPS. The partnership will be regarded as a person separate from its partners under the DPS Ordinance and is entitled to compensation up to a maximum of HK$800,000 on its own.

Are deposits held by an association, society, club, or other unincorporated entities protected by the DPS?

Yes. Each separate legal entity will be protected up to a maximum of HK$800,000.

Are deposits held in a trust account or a client account protected by the DPS?

Yes. Deposits held in trust and client accounts are protected by the DPS. The DPS Ordinance has laid down clear rules on how such deposits are protected.

Who are excluded from the protection of the DPS?

According to the DPS Ordinance, several types of persons (the excluded persons) are not protected by the DPS:

- a related company of the Scheme member

- a multilateral development bank as defined in section 2(1) of the Banking Ordinance

- an authorized institution, i.e. licensed banks, restricted licence banks and deposit-taking companies

- a foreign bank which is not an authorized institution in Hong Kong

- the senior management, controllers and directors of the Scheme member and its related companies

Financial products protected by the DPS

What financial products are protected by the DPS?

Only deposits held with Scheme members are protected by the DPS. Other financial products such as bonds, stocks, warrants, mutual funds, unit trusts, insurance policies and virtual assets are not protected by the DPS.

Is it possible that the protection status of similar products offered by different banks can be different?

Yes, it is possible because the products offered by different banks may have different terms and conditions, and hence their protection status may be different. Banks are required to disclose whether your deposits are protected or not. In case of doubt, you may ask your bank about the protection status of a particular product.

Does the DPS protect the valuables kept in my safe deposit box opened with a Scheme member?

No. They are not protected by the DPS.

What is a secured deposit? Is it protected?

A secured deposit means a deposit pledged to a bank, normally for the purpose of obtaining a credit facility from the bank. Yes, it is protected by the DPS.

What is a structured deposit? Why are structured deposits not protected by the DPS?

Structured deposits can take many different forms. Typical examples of structured deposits are foreign currency linked deposits and equity linked deposits. The amounts of principal and / or interest to be repaid for such deposits are linked to the performance of the underlying financial assets.

The nature of structured deposits is more akin to an investment rather than a deposit. As such, a common practice in other jurisdictions (such as Canada and some European countries) is to exclude such products from the scope of deposit protection. Hence, all structured deposits are currently excluded from DPS protection.

What is a bearer instrument? Why are bearer instruments not protected by the DPS?

A bearer instrument, in simple terms, is a financial instrument where the holder of the instrument is entitled to the repayment of the money underlying the instrument. A typical example of a bearer instrument is a bearer certificate of deposit, where the holder of the certificate evidencing the deposit is entitled to the repayment of the principal from the issuing bank, whether or not he or she is the person who made the deposit at the beginning.

As it is not possible to verify the beneficial owners of the bearer instruments within a short period of time, it is a common international practice to exclude such instruments from the scope of deposit protection.

A term deposit with a maturity exceeding 5 years is not protected. How is the term to maturity determined?

The DPS does not protect time deposits with a maturity exceeding 5 years. The term to maturity of a deposit refers to the current term agreed to by the depositor at the most recent time the deposit was negotiated. It does not refer to the remaining maturity of a deposit. For example, a 6-year term deposit placed with a Scheme member will not be protected by the DPS although the deposit will mature in 3 years.

What is an off-shore deposit? Why are offshore deposits not protected by the DPS?

Off-shore deposits refer to deposits placed with overseas branches of Scheme members. As the funds reside in the banking system of an overseas jurisdiction, it falls outside the scope of coverage of the DPS.

How can I know whether a financial product is protected by the DPS?

You can ask the bank offering the financial product to you whether it is protected by the DPS.

Disclosure and Representations

Will I be notified if my deposit is not protected by the DPS?

Your bank will notify you and obtain your acknowledgement before each transaction of a non-protected financial product that has been described as a deposit but is not protected by the DPS. Nevertheless, if the transaction is made by an institutional customer, a private banking customer or is related to money placed into accounts for payment purposes, the bank can instead notify the relevant customer when the account is opened and at least once a year afterwards.

Will I be notified if my deposit is qualified for protection under the DPS?

In general, your bank will notify you that the deposit is protected before the account is opened or when deposit is made, or within a period of 30 days from the date on which the account is opened or the deposit is placed.

Compensation

How will the compensation amount be calculated?

Compensation will be calculated in gross amount. All deposit accounts held by the same depositor in a bank will be aggregated for calculating the compensation, subject to the HK$800,000 protection limit.

Does the DPS protect interest on deposits?

Yes. Interest accrued on a protected deposit is covered by the DPS.

Will I receive compensation in foreign currencies in respect of my foreign currency deposits?

No. All compensation under the DPS will be paid in Hong Kong dollars. The Board will convert foreign currency deposits into Hong Kong dollars in determining the entitlement to compensation of depositors.

Under what circumstances will compensation be paid by the DPS?

Compensation will be paid when (i) the Court issues a winding-up order to a Scheme member; or (ii) the Monetary Authority, after consultation with the Financial Secretary, instructs the Board to pay compensation.

Will I be notified if compensation under the DPS has become payable?

When compensation under the DPS is triggered in respect of a Scheme member, the Board will inform the depositors of the Scheme member by notice published in major newspapers or by a means which the Board considers appropriate under the prevailing circumstances.

How long does it take for the Board to pay compensation to affected depositors?

The Board will pay compensation to affected depositors as soon as practicable in the event of a bank failure. The exact timing will however vary from case to case. In general, the Board has a target of seven days in making payments to depositors.

What should I do if my bank failed?

Depositors do not need to file a claim with the Board. The Board will examine the records of the Scheme member to identify eligible depositors and calculate the compensation amounts.

Can I appeal if I am not happy with the compensation amount?

You should first contact the Board and ask for an explanation. However, if a depositor is still not satisfied with the compensation amount, he or she may appeal to the Deposit Protection Appeals Tribunal. The contact details of the Tribunal are as follows:

Address :

Room 702, Tower Two, Lippo Centre, 89 Queensway, Hong Kong

Telephone : 2912 8553

Fax : 2524 7097

Enhanced deposit protection in the event of a merger or acquisition involving Scheme members

Why is there enhanced deposit protection in the event of a bank merger or acquisition?

The enhanced deposit protection aims to provide a transitional period for depositors affected by bank mergers or acquisitions to consider if they wish to adjust their deposit portfolios (e.g. reallocating part of their deposits to another bank) to bring their deposit balances under the standard protection limit. Specifically, each affected depositor will have an additional coverage for his/her protected deposits transferred from each of the original Scheme member(s) up to the standard protection limit, on top of the standard protection limit available at the resulting Scheme member, where applicable. The enhanced deposit protection will generally last for six months from the effective date of the bank merger or acquisition.

Who will be eligible for enhanced deposit protection under the DPS?

A merger or acquisition involving a transfer of protected deposits among two or more Scheme members taking effect on or after 1 January 2025 is a qualifying arrangement under the DPS. If you have pre-existing protected deposits with two or more Scheme members involved in a qualifying arrangement immediately before the date of merger or acquisition, you will be eligible for enhanced deposit protection for a time-limited period after the effective date of merger or acquisition.

What will be the maximum level of deposit protection for affected depositors in a qualifying merger or acquisition arrangement under the DPS?

If you have pre-existing protected deposits with two or more Scheme members immediately before the date of merger or acquisition, you will, for a period of six months from the effective date of merger or acquisition, have an additional coverage for your protected deposits transferred from each original Scheme member up to the standard protection limit, on top of the standard protection limit available at the resulting Scheme member.

In case a time deposit with original maturity date beyond the six-month period is involved, the enhanced protection period for the time deposit will be until its original maturity date. For the avoidance of doubt, if a time deposit matures within the six-month period and is renewed with the relevant Scheme member, the additional coverage will still apply only up to the end of the six-month period.

If I have deposits with the Scheme members involved in a merger or acquisition, do I need to apply or pay for the enhanced deposit protection under the DPS?

No, you do not need to apply or pay for the enhanced deposit protection as the enhanced coverage for protected deposits is automatically provided for affected depositors under the law.

If I have deposits with only one, but not both, of the Scheme members involved in a merger or acquisition, am I entitled to the enhanced deposit protection?

As you have pre-existing protected deposits with only one of the Scheme members involved in a merger or acquisition, the maximum level of deposit protection before and after the merger or acquisition will remain at the standard protection limit.

Will the maximum level of deposit protection be adjusted if there are changes to the amount of deposits during the six-month period after a bank merger or acquisition?

The enhanced deposit protection limit will remain unchanged for six months after a bank merger or acquisition regardless of any changes to the amount of deposits during the six-month period.

Will I be notified of the enhanced deposit protection arrangement if my banks are involved in a qualifying merger or acquisition arrangement?

Scheme members involved in a qualifying merger or acquisition arrangement are required to, on or before the merger or acquisition takes effect, notify affected depositors about the enhanced deposit protection arrangement, such as the types of depositors eligible for the enhanced deposit protection, description about the enhanced deposit protection, the effective date of merger or acquisition (an indicative or target date may be provided by a Scheme member if the effective date is not yet confirmed at the time of issuance of the notice), and the duration of the enhanced deposit protection.

Do I need to maintain relevant deposit records as at the date of merger or acquisition to prove that I am entitled to enhanced deposit protection just in case the resulting Scheme member fails?

No, you do not have to maintain deposit records as at the date of merger or acquisition, as the resulting Scheme member will be required to maintain such records.